Call Today for a FREE Consultation

210-342-3400

Recent Blog Posts

Can the Government Seize Social Security Checks to Pay for Delinquent Student Loans?

When most people think of student loan debt, they usually picture someone who has recently graduated from college within the past few years, who, along with that diploma they earned, now owes thousands and thousands of dollars in student loans. Many young adults can be so overwhelmed with student debt, with threats of wage garnishments and other heavy-handed collection tactics, that they are unable to pay their other bills. Quite often, the only option they have to get out from all that debt is to file bankruptcy. Although student loans cannot be discharged in bankruptcy, other debts can, and this may free enough income for them to be able to afford their monthly student loan payments.

When most people think of student loan debt, they usually picture someone who has recently graduated from college within the past few years, who, along with that diploma they earned, now owes thousands and thousands of dollars in student loans. Many young adults can be so overwhelmed with student debt, with threats of wage garnishments and other heavy-handed collection tactics, that they are unable to pay their other bills. Quite often, the only option they have to get out from all that debt is to file bankruptcy. Although student loans cannot be discharged in bankruptcy, other debts can, and this may free enough income for them to be able to afford their monthly student loan payments.

But it is not just young adults who are being buried with student loan debt. More and more older people, including the elderly, are struggling with it. It is estimated that approximately seven million Americans over the age of 50 have student loan debt.

Best Use of Your $1,400 Stimulus? Bankruptcy!?

You no doubt have countless uses for the next stimulus payment. But if you are like some people, the very best use is to file bankruptcy. Like who?

Last week Congress passed the American Rescue Plan Act and President Biden signed it into law. Among its many parts is the $1,400 per person stimulus payment—officially called the Economic Impact Payment. On Friday, March 12, 2021, the IRS put out a news release about these payments. This provides general information about qualifying for the payments, and the amounts individuals and families will receive. There are more details in this IRS Fact Sheet. For information on your own payment, “[b]eginning Monday [March 15], people can check the status of their third payment by using the Get My Payment tool . . . .”

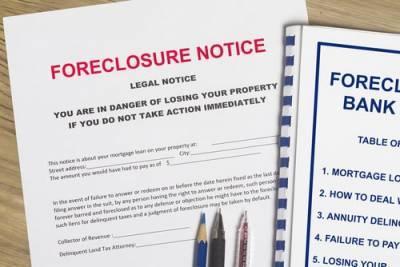

Chapter 13 Bankruptcy Helps You Sell Your Home

Chapter 13 bankruptcy enables you to use the pandemic’s mortgage payment forbearance process and sell your home if and when you are ready to do so.

Last week we showed how Chapter 7 helps you take advantage of the pandemic foreclosure moratorium when selling your home. Today we show how it works even better with the more powerful Chapter 13 “adjustment of debts.”

In the last few weeks, there has been an important related development. The Biden Administration extended the foreclosure moratorium deadline by three months, from March 31 to June 30, 2021. This also extended the mortgage payment forbearance request window until June 30, and potentially lengthened certain ongoing forbearances. White House Fact Sheet, February 16, 2021.

FAQs Surrounding the Foreclosure Process in Texas

It is extremely difficult to face foreclosure. You may feel angry, upset, and frustrated, and all of those feelings are to be expected. However, if you are in danger of losing your home, it is important to remain calm and to understand how the process works. This is the only way to identify any potential defense you may have, which will give you the best chance of keeping your home. To learn more, our attorneys have created a list of the most frequently asked questions they are asked about foreclosure, and the answers to them.

It is extremely difficult to face foreclosure. You may feel angry, upset, and frustrated, and all of those feelings are to be expected. However, if you are in danger of losing your home, it is important to remain calm and to understand how the process works. This is the only way to identify any potential defense you may have, which will give you the best chance of keeping your home. To learn more, our attorneys have created a list of the most frequently asked questions they are asked about foreclosure, and the answers to them.

Is Texas a Judicial Foreclosure State?

Most foreclosures in Texas are non-judicial. This means that when a borrower defaults on their mortgage, the lender can foreclose on the home without first filing a lawsuit against them and going to court. Non-judicial foreclosure is only available when the mortgage deed contains a Power of Sale clause. When a mortgage loan does include a Power of Sale clause, the borrower has already agreed that the lender can foreclose on the home in the event that they default on the mortgage.

Bankruptcy Basics: Chapter 7 vs. Chapter 13

When you are swimming in debt, ignoring phone calls from creditors, facing a repossession or foreclosure, and your mailbox is filling up with lawsuits and letters from collectors, it can feel as though your life is spinning out of control. But, is bankruptcy really the right debt solution for you? And if it is, which personal bankruptcy option should you choose? While there are a number of factors to consider in reaching the answers to those questions, and a qualified attorney is best suited to guide you, the following information on bankruptcy basics will help you understand the basics.

When you are swimming in debt, ignoring phone calls from creditors, facing a repossession or foreclosure, and your mailbox is filling up with lawsuits and letters from collectors, it can feel as though your life is spinning out of control. But, is bankruptcy really the right debt solution for you? And if it is, which personal bankruptcy option should you choose? While there are a number of factors to consider in reaching the answers to those questions, and a qualified attorney is best suited to guide you, the following information on bankruptcy basics will help you understand the basics.

Common Types of Personal Bankruptcy

Both Chapter 7 and Chapter 13 bankruptcies allow you to manage or eliminate unsecured debts and stop the proceedings of foreclosures, garnishments, repossessions, utility shutoffs, and debt collections. However, child support, alimony, fines, some types of back taxes, and most student loan debts may be exempt, leaving you still obligated to pay them. Additionally, both may allow you to keep certain assets (within your state’s maximum valuation), such as a car or primary residence. But, this is where the similarities for the types of bankruptcies end.

Preparing for Personal Bankruptcy in Texas

The decision to file for personal bankruptcy is not one that is easily made. Moreover, the days, weeks, and months following the decision can also be difficult, as there may be feelings of fear or concern. Then there is still the stress of preparing for the bankruptcy process. The following may be able to help alleviate some of that stress and provide guidance on how to find the assistance you need.

Start by Contacting an Attorney

While there are many steps to take during the bankruptcy process, your first should be to contact an experienced bankruptcy lawyer. Not only does this help you prevent missteps during the bankruptcy process, but it can also expedite the next steps. By contacting a lawyer, you can get you on your way to less stress from the creditor calls and collection letters.

Cancel Your Automatic Payments

If you are like most consumers, you have automatic payments that are drafted from your account. Some might be for subscriptions while others might be with creditors, all should be eliminated. This can help you start to step forward and manage your debt more responsibly. It also gives you more control over what you are paying in the weeks leading up to the bankruptcy filing.

Debunking Four Common Bankruptcy Myths

There are many negative perceptions about bankruptcy. On one hand, some of these perceptions are well-deserved. After all, there are some potential drawbacks to filing. Yet there are also some major misconceptions about bankruptcy—some of which could keep someone from filing when they really should. The following information is designed to debunk these bankruptcy myths. It may even help you decide what your next step should be, and if bankruptcy might be the right solution for you.

There are many negative perceptions about bankruptcy. On one hand, some of these perceptions are well-deserved. After all, there are some potential drawbacks to filing. Yet there are also some major misconceptions about bankruptcy—some of which could keep someone from filing when they really should. The following information is designed to debunk these bankruptcy myths. It may even help you decide what your next step should be, and if bankruptcy might be the right solution for you.

Myth 1: Bankruptcy Ruins Your Credit Forever

True, your credit can take a hit after filing for bankruptcy, and it may be difficult to obtain new lines of credit once the process starts, but bankruptcy does not completely ruin your credit. If anything, it gives you a clean slate to start over. It is also usually less damaging than continuing to make late payments on your debts. If you are still a little apprehensive about filing, talk to a qualified bankruptcy attorney for a comprehensive analysis of your financial situation.

Settling Debt with Your Creditors After a Hardship

Life can be unpredictable. Life can be messy and complicated. And, sometimes, the worst things that can happen to us are completely out of our control. But what do you do when the messy, unpredictable, and complicated lead to financial problems? How do you turn things around and regain control of your financial future? The answer really depends on where you are in the debt collection process. While some may be able to find a viable bankruptcy alternative, others may need more aggressive action. The following information may be able to help you in determining your best course of action for settling debt with creditors.

Creditor Harassment with No Negative Actions

If you have only just started being hounded by your creditors and have not yet received any notice of wage garnishment, tax or property liens, bank seizures, home foreclosure, or any other negative actions against you, you may be able to negotiate a repayment plan with your creditors. But, because not all creditors are willing to work with consumers, and because they have no incentive to actually help you, it may take the assistance of a skilled attorney to resolve the matter before things escalate.

Bankruptcy Timing for Vehicle Cramdown

Cramdown usually lowers your monthly vehicle loan payment and the total amount you must pay. To qualify the loan must be more than 910 days old.

We’re in the midst of a series on filing your bankruptcy case with the best timing. Today we get into the right timing to be able to cram down your vehicle loan. Cramdown is a potentially huge benefit, so it’s important to know how to take advantage of it. One key consideration in this is the timing of your bankruptcy filing.

Advantages of Vehicle Loan Cramdown

In a Chapter 7 “straight bankruptcy” case, if you have a vehicle loan you must “take it or leave it.” To keep the vehicle, you have to “reaffirm” the vehicle loan. That means you agree to remain fully liable on the debt. It usually means you are stuck with the regular monthly payment, even if you can’t afford it. You can’t change the interest rate, even if it’s high, and jacking up how much you must pay. You are stuck with the full balance on the loan, even if the vehicle is worth much less. This includes late fees and any other contractual charges. If you’re behind almost always you have to quickly catch up. Usually, the only other choice is to “leave” it—surrender the vehicle and discharge (write-off) the vehicle’s debt. If you need and want to keep your vehicle, that’s not an option.

Chapter 13 Timing to Discharge Student Loans

Discharging a student loan requires meeting the difficult condition called undue hardship. Chapter 13 can help through more flexible timing.

We’re in a series on the best timing for filing your bankruptcy case. Two weeks ago we introduced the special condition you have to meet to discharge (write off) student loans: undue hardship. Last week we focused on how to better meet that condition with smart timing of a Chapter 7 “straight bankruptcy” case. Today we get into doing that with a Chapter 13 “adjustment of debts case.

Undue Hardship Requirements

We’re focusing on the phrase “undue hardship” because the law clearly establishes that as a condition for discharging student loans. The U.S. Bankruptcy Code says you can’t discharge a student loan unless paying it “would impose an undue hardship on the debtor [you] and the debtor’s dependents.” Section 523(a)(8). Generally bankruptcy courts have interpreted “undue hardship” to include three requirements. Each has a timing consideration. We’ll look at these three, showing how the timing benefits of Chapter 13 case can help you meet them.

Call Today for a FREE Consultation

210-342-3400